Japanese Venture Ecosystem

- Erdinc Ekinci

- Apr 30

- 13 min read

JAPAN RADAR — TOKYO EDITION

A Co-Capital Ecosystem Report · Edition 01 · May 2026

ABOUT THIS REPORT

The Japan Radar is an ecosystem intelligence series produced by Co-Capital. Each edition examines a specific venture ecosystem — its capital, its people, its corridors, and the dynamics that shape what gets built there. This first edition focuses on Tokyo, with broader Japan context. Future editions will cover Osaka, Fukuoka, Kyoto, and other Japanese hubs, followed by editions on Korea, Taiwan, and the cross-border corridors connecting them.

The accompanying Investor & Ecosystem List (separate spreadsheet) contains the comprehensive directory of venture capital firms, corporate venture capital (CVC) units, accelerators, incubators, government and university-affiliated capital, and the most active people shaping the Japanese venture ecosystem as of early 2026. Each entry includes source citations.

METHODOLOGY

This report was assembled using a combination of:

Public secondary sources — published industry data from Tracxn, Chambers and Partners (Venture Capital 2025 — Japan), JETRO, the Japan Venture Capital Association directory, IMARC Group, StartupBlink Global Startup Ecosystem Index 2025, Coral Capital's published commentary, Disrupting Japan podcast transcripts, and Crunchbase / Tracxn investor profiles.

Cross-referenced firm directories — Failory, OpenVC, BaseTemplates, IncubatorList, Shizune, Visible.vc, and Growth List, used to triangulate active investor lists with portfolio activity in the past 12–24 months.

First-hand observation — operational presence in Tokyo through Founder Institute Japan, Korea, and Taiwan chapters, in-person events, and direct engagement with Japan-based and cross-border investors.

Inclusion criteria for the investor list: entities are listed if they (a) have made at least one disclosed investment into a Japan-based startup in the past 24 months, (b) maintain a Japan office or dedicated Japan investment activity, or (c) are explicitly named in published industry directories as active in the Japanese market. Each entry includes a source citation.

Limitations: the venture capital ecosystem changes continuously. Funds raise new vehicles, partners move, CVCs reorganize, and angel investors enter and exit at high frequency. This list reflects the publicly verifiable picture as of early 2026. Where we are uncertain, we say so.

TABLE OF CONTENTS

Why Tokyo, Why Now

The Macro Numbers

The Three Tokyos: How the Ecosystem is Geographically Organized

What's Actually Happening on the Ground

Cross-Border Corridors

Active Startup Regions Across Japan

Hidden Opportunities

Tokyo Ecosystem Heat Score

Closing — and What's Next

For the comprehensive list of firms, programs, and people active in the Japanese ecosystem, see the accompanying Investor & Ecosystem List spreadsheet.

1. WHY TOKYO, WHY NOW

Japan is simultaneously respected, underestimated, technologically influential, culturally powerful, economically complicated, and venture-conflicted. That tension is exactly what makes this ecosystem interesting to cover right now.

For roughly two decades after the asset bubble burst, Japan's venture capital activity remained small relative to the size of its economy. Investment flowed through banks, into corporates, and into stable mid-cap businesses. Startups existed, but the supporting infrastructure — risk-tolerant LP capital, equity-incentivized employees, foreign founders; did not. The ecosystem was, in a phrase widely used by people who lived through it, "a black box."

That has changed materially in the last decade, and it has accelerated since 2022. Annual venture investment into Japanese startups grew from roughly USD 500 million in 2012 to approximately USD 23.5 billion in 2025, according to IMARC Group. The Japanese government formally launched a five-year Startup Development Plan in 2022 with an aspirational target of 100,000 startups and 100 unicorns by 2027, and committed JPY 10 trillion (approximately USD 67 billion at current rates) to support it.

The result is an ecosystem with more capital, more corporate engagement, more government backing, and more international attention than it has ever had; yet still working through the structural questions of whether that capital is producing globally-scaling companies.

Tokyo is where the answer to that question is being written. Approximately 73% of all Japanese startup funding flows through Tokyo, according to Growth List's 2026 ecosystem analysis, and the city hosts roughly 9,000 startups — about nine times the count of any other Japanese city. Understanding Tokyo is, for practical purposes, understanding the Japanese venture ecosystem.

2. THE MACRO NUMBERS

Seven numbers that define the current state of the Japanese venture market:

USD 23.5 billion — estimated size of the Japanese venture capital investment market in 2025, per IMARC Group, with projected growth at a 16.71% CAGR through 2034.

~41,000 active startups — total registered startups in Japan as of January 2026, per Tracxn. Of these, approximately 10,100 are funded.

USD 89.9 billion — cumulative venture capital and private equity raised by Japanese startups across all funding rounds, per Tracxn.

73.4% — Tokyo's share of all Japanese startup funding, per Growth List 2026.

11 unicorns — confirmed Japanese unicorns as of early 2026, per Tracxn. CB Insights' State of Venture 2024 Report counted 8 Japanese unicorns out of 1,250 globally as of end-2024.

400+ corporate investors — Japanese corporations now actively investing in startups, more than double the 2018 number, per Growth List.

JPY 10 trillion — total committed government investment under the Startup Development Five-Year Plan (2022–2027).

The numbers tell two stories simultaneously. One story is dramatic growth: the Japanese venture market multiplied roughly 13x in a decade, government commitment is genuinely large and durable, and corporate engagement has more than doubled. The other story is the unicorn gap: Japan, with the world's third-largest economy, has produced fewer unicorns than Korea, despite Korea's GDP being roughly one-third of Japan's.

The unicorn gap is the most-misread number in Japanese venture. Japan's IPO market is structurally easier to access than the US market, with companies that would remain private until decacorn status in San Francisco listing publicly at JPY 30–80 billion (roughly USD 200–550 million) valuations on the Tokyo Stock Exchange Growth Market. Japan recorded approximately 50 IPOs in 2025 and 125 IPOs in 2024 — a higher per-capita exit volume than most developed venture markets. Counting unicorns systematically undervalues the actual exit performance of the ecosystem.

3. THE THREE TOKYOS: HOW THE ECOSYSTEM IS GEOGRAPHICALLY ORGANIZED

Tokyo's startup ecosystem is not one community but three overlapping ones, each with its own geography, language defaults, and decision speeds. Understanding which "Tokyo" a person operates in tends to predict more about their behavior than their formal title.

Tokyo One: The Shibuya–Roppongi axis. This is the globally-oriented, English-friendly part of the ecosystem. Most foreign-friendly accelerators and venture capital firms operate from this corridor. Notable startup hubs include Shibuya QWS, the recently expanded Toranomon Hills Innovation District, and the cluster around Roppongi Hills. If a foreign founder or visiting investor only sees one part of Tokyo's ecosystem, this is the part they see — Shibuya is reasonably described as the closest Tokyo equivalent to the SoMa or Mission districts of San Francisco in terms of startup density.

Tokyo Two: The Otemachi–Marunouchi axis. This is the corporate venture core, the heart of Japan's institutional finance, and the geographic home of most corporate venture capital activity. The major bank-affiliated venture vehicles, insurance company venture arms, and corporate innovation programs run out of this district. Decisions move more slowly here, capital is patient, and the relationship horizons are measured in decades rather than years. For a startup with strategic-distribution needs (a fintech needing banking partnerships, an insurtech needing carrier relationships, an industrial AI startup needing a manufacturing partner), Otemachi is where the structurally important conversations happen.

Tokyo Three: The Hongo–Kashiwa axis. This is the deep-tech and university spin-out belt, anchored around the University of Tokyo's Hongo and Kashiwa campuses. The University of Tokyo's investment platform, several deep-tech specialist VCs, and the broader cluster of academically-affiliated investors operate here. The companies that emerge from this corridor are slower-moving but technically extraordinary — most of Japan's globally-significant deep-tech businesses originated in or near this cluster.

The strategic implication for foreign founders, investors, and ecosystem participants: most newcomers get routed to Shibuya first because it's the only one of the three Tokyos with English-language entry points. Staying only in Shibuya means missing both the deepest capital pools (Otemachi) and the most defensible technology (Hongo). The most sophisticated operators in Tokyo move fluently across all three.

4. WHAT'S ACTUALLY HAPPENING ON THE GROUND

Six observations from operating inside the Tokyo ecosystem in 2025–2026 that don't typically appear in published market reports:

The capital is here. The founder density is not. Japan's binding constraint is no longer money. Government funds-of-funds, Japan Investment Corporation, NEDO, the 400+ corporate CVCs, and the growing presence of foreign capital have made early-stage funding genuinely available for credible teams. The constraint is the supply of ambitious founders willing to attempt globally-scaling companies rather than mid-cap domestic IPOs. This has been a consistent message from leading Japanese venture investors: bringing more foreign capital into Japan will not, by itself, fix a supply-side problem.

Foreign founders still face a structurally harder fundraise pre-traction. Japan is opening up. Visa reforms have eased the path to founder residency, English-language startup events are more numerous than ever, and high-profile foreign-led wins have shifted the narrative significantly. But for a foreign founder without traction, raising a seed round in Tokyo remains meaningfully harder than raising a comparable round in Singapore, San Francisco, or even Dubai. Most domestic Japanese VCs default to Japanese-speaking teams, partly because they themselves operate primarily in Japanese and partly because their portfolio support and follow-on networks are Japanese-language. The exceptions — a small cluster of foreign-friendly independents, several US-affiliated firms, and a small number of CVCs with explicit cross-border mandates — make up most of the foreign-founder funding map.

Corporate decision timelines have not compressed to AI timelines. Japanese corporates are now more active in startup investment and POCs than ever, but their decision cycles have not adapted to the speed of modern AI-native startups. A six-month POC discussion with a major manufacturer is still common. AI-native startups operating on six-week iteration cycles find this structurally painful. The arbitrage opportunity is real for founders who can package bilingual sales materials and run a Japan-specific commercial motion that respects the timeline difference.

AI tooling has dramatically lowered the technical-prototyping barrier for foreign founders. Foreign founders without a Japanese co-founder previously needed months to ship a localized product, with the localization layer (UI translation, business-document generation, customer support) being a hard manual cost. Modern AI tooling has compressed this from a months-long workstream to a weeks-long one. The bottleneck for many foreign-founded startups in Tokyo has shifted from build to distribution.

Government support exists but is fragmented. J-Startup, JETRO, METI, NEDO, JIC, the Tokyo Metropolitan Government's Startup Hub Tokyo, and various regional programs all offer meaningful support for startups. The aggregate is significant. But these programs are not centrally coordinated, English-language information is patchy, and founders typically discover them sequentially rather than systematically. There is a genuine ecosystem-connector role still to be built here.

The next Japanese wave is industrial AI, not consumer apps. Japan's structural strengths — manufacturing, robotics, materials science, semiconductors — are becoming software-defined faster than most international observers realize. The next generation of Japanese global champions is more likely to emerge from this physical-AI corner than from consumer SaaS. The cluster of robotics, materials, and manufacturing AI startups represents the gravitational pull of where Japan's structural advantages are converting into venture-scale opportunities.

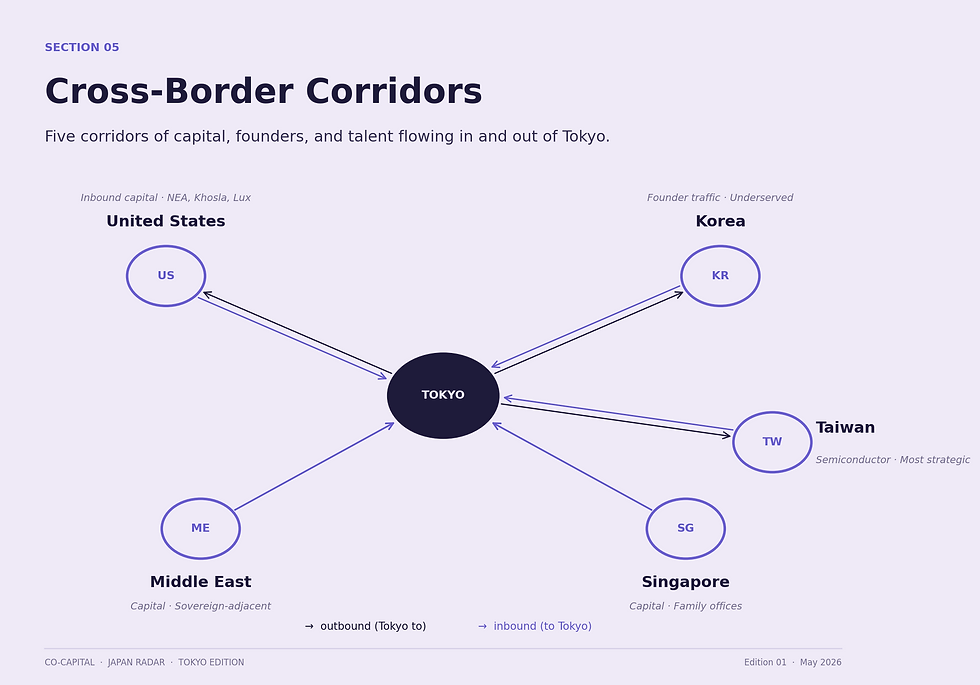

5. CROSS-BORDER CORRIDORS

Tokyo's relationship with the rest of the world is increasingly structured through five distinct corridors. Each has its own dynamics, its own bridge institutions, and its own gaps.

Japan ← United States (inbound capital). This is the most visible and rapidly densifying corridor. Top-tier US firms — NEA, Khosla Ventures, Bessemer Venture Partners, Lux Capital, Founders Fund — have stopped treating Japan as exotic. The Sakana AI Series C, led by NEA, Khosla, and Lux, was the moment this became uncontroversial. Late-stage growth capital from KKR, General Atlantic, and Ontario Teachers' Pension Plan is now routinely deployed into Japanese growth-stage companies. What remains rare: US firms leading seed rounds in Japan without a local co-investor. A handful of bridge funds continue to function as the trusted intermediaries.

Japan → United States (outbound expansion). The harder direction. Japanese startups expanding to the US tend to succeed when they have either a foreign co-founder, a US-based partner, or a corporate parent with US presence. We expect this corridor to densify as the Tokyo-SF bridge model gets replicated.

Japan ↔ Korea. Underserved relative to its strategic importance. Korea has produced more unicorns per dollar of GDP than Japan, and there is increasing two-way founder traffic — particularly in consumer, gaming, and AI. Korean founders looking to scale into Japan typically use Tokyo as a staging point for the broader Asian rollout. Few institutional bridges exist; the corridor is largely founder-to-founder and operator-to-operator at present.

Japan ↔ Taiwan. The most strategically important corridor that remains under-covered in English. Taiwan's semiconductor and hardware density, combined with Japan's industrial and AI infrastructure investments — including the Japanese government's JPY 100 billion commitment to Rapidus for next-generation domestic semiconductor production — makes this corridor structurally critical for the next decade. Few investors are explicitly positioned across both ecosystems. The Founder Institute Taiwan chapter, operating alongside the Japan and Korea chapters, is one of the few systematic bridges.

Japan ↔ Singapore / Middle East. This is more of a capital corridor than a founder corridor. Singapore-based family offices and Dubai- and Riyadh-adjacent capital are increasingly looking at Japan as a stable, yen-denominated diversification play. Most have not yet found their preferred landing pad. The institutional infrastructure to absorb this capital efficiently in Tokyo is still being built.

6. ACTIVE STARTUP REGIONS ACROSS JAPAN

Tokyo is the gravitational center, but the rest of Japan is meaningful and growing. Brief notes on the four other regions worth knowing — full editions on each are planned.

Osaka. Japan's second-largest startup ecosystem, with growing momentum around Osaka Innovation Hub and the Kansai region's traditional manufacturing base. Strong in life sciences, manufacturing tech, and B2B SaaS targeted at the Kansai industrial complex. Hosting Expo 2025 has materially accelerated startup-related infrastructure and visibility.

Fukuoka. Frequently cited as Japan's most founder-friendly city outside Tokyo, partly due to municipal initiatives including the Fukuoka Startup City designation and the dedicated startup visa program. Strong concentration in consumer, e-commerce, fintech, and globally-oriented software. Significantly lower cost of living and operations than Tokyo.

Kyoto. Smaller in volume but disproportionately important in deep tech, particularly in fusion, materials science, and university spin-outs from Kyoto University. The cultural anchor for a particular kind of patient, technically-deep founding team.

Nagoya and the Tokai region. The Toyota-anchored industrial hub, with a growing deep-tech and mobility startup cluster. Central Japan Innovation Capital launched its first dedicated venture fund in late 2024, targeting Tokai-region deep-tech and university ventures with backing from Aichi Prefecture, Nagoya City, and regional financial institutions.

Each of these will receive its own dedicated Radar edition.

7. HIDDEN OPPORTUNITIES

Sectors and structural opportunities that are under-built relative to the size of the addressable problem in Japan.

Industrial AI for SMBs. Japan has approximately 3.6 million small and medium-sized enterprises, most operating in manufacturing, logistics, or services with decades-old workflow systems. AI tooling that wraps existing ERP and shop-floor systems with a Japanese-native UX is a large under-served opportunity. Most VC attention is on enterprise AI; the SMB tier is being almost entirely missed.

Aging-population software. Japan has the oldest population on earth and the most aggressive demographic curve. Healthcare staffing, in-home-care logistics, and elderly-care SaaS are structurally guaranteed to grow for the next thirty years. The cultural and empathy bar is lower than for consumer-facing products, making this a relatively accessible category for foreign founders with healthcare backgrounds.

Defense and dual-use technology. Japan's defense posture has shifted materially since 2022. Government appetite for dual-use technology investment is at a generational high. In-Q-Tel's participation in Sakana AI's Series B is one of the more striking signals. This sector is opening from near-zero startup activity in 2020 to being one of the most strategically funded by 2027.

Manufacturing AI and physical-world models. Japan has the world's deepest manufacturing dataset and the world's best-instrumented factories. The companies that train the next generation of physical-world AI models — industrial vision, robotics policy networks, materials simulation — will need access to this data. Japan-based founders have a structural moat here that is barely being exploited.

Talent and immigration tooling. Japan has stated a need to import substantial foreign labor over the coming decades to maintain its workforce. Visa, onboarding, language acquisition, housing, and cultural integration tooling for migrant workers is a guaranteed-growth category that is almost entirely unbuilt.

Cross-border GTM-as-a-service. Most Japanese startups want to expand globally; most foreign startups want to expand into Japan. Both sides are under-served. The companies that build the operational layer — entity setup, hiring, compliance, localization, distribution — for this two-way flow will compound for a decade.

AI-native vertical B2B SaaS for the long-tail Japanese enterprise. SmartHR proved the model. There are likely 20–30 more SmartHR-shaped categories — vertical B2B SaaS where the Japanese workflow is genuinely different from the US workflow and requires a Japan-native product. Each of these is plausibly a USD 500 million to USD 1 billion company waiting to be built.

8. TOKYO ECOSYSTEM HEAT SCORE

Co-Capital's qualitative scoring of the Tokyo ecosystem across nine dimensions, on a 1–10 scale. Updated each Radar edition. These are calibrated estimates, not surveyed metrics.

Dimension | Score | Reasoning |

Capital availability | 8 | Substantial domestic and growing foreign capital across stages |

Founder friendliness (domestic) | 7 | Improving rapidly; J-KISS and stock option reforms have helped |

Foreign founder accessibility | 5 | Improving but still significantly behind Singapore or Dubai |

Speed of business | 4 | Corporate timelines remain a structural friction |

AI readiness | 7 | Strong infrastructure investment; fragmented enterprise adoption |

Government support | 8 | Genuinely large, durable, and policy-backed |

Global connectivity | 6 | Improving; foreign capital and talent flows are densifying |

Talent density | 7 | Strong technical and engineering talent; thinner in commercial scaling |

Exit potential (IPO + M&A) | 9 | Among the most accessible IPO markets in the developed world |

How to read this: Tokyo's strongest scores — exit potential, government support, capital availability — reflect a structurally mature ecosystem. The IPO market is more accessible than almost any other developed market, government commitment is large and durable, and capital is now abundant at every stage from seed through growth. Tokyo's weakest scores — speed of business, foreign founder accessibility, global connectivity — represent the unfair-advantage gaps for any operator who can solve them. The language barrier is real. Corporate decision speed is real. The default-Japanese-only founder pipeline is real. Each of these is improving year-over-year, and founders or investors who position around these gaps in 2026 are likely to compound through 2030.

9. CLOSING — AND WHAT'S NEXT

Generic AI-generated ecosystem reports are dead on arrival. The reason this Radar can exist is that the people producing it are physically embedded in the ecosystem they describe — through Founder Institute chapters in Japan, Korea, and Taiwan, through Openfor.co's incubator programs, and through Co-Capital's content and community work across Asia.

The intent is not to publish a one-time report. The intent is to build a living signal layer across the venture ecosystems we operate inside — one that updates as the ecosystem updates, features the people who actually move it, and becomes more valuable over time as the cross-border picture becomes clearer.

The next Japan Radar editions will go deep on Osaka, Fukuoka, Kyoto, and the Tokai region. After that, we expand to Korea Radar, Taiwan Radar, Silicon Valley Radar from a Japan perspective, and Middle East Radar — covering the cross-border corridors that we sit on most directly.

The accompanying Investor & Ecosystem List spreadsheet is provided as a separate file. It contains the comprehensive directory of firms, programs, and the most active 30 people shaping the Tokyo ecosystem, with sources for each entry. It is intended to be updated quarterly. We welcome corrections, additions, and suggestions from anyone operating in the Tokyo ecosystem — the data is as good as the network feeding it.

If you are building, investing, or operating in any of the ecosystems Co-Capital covers and would like to be featured, contribute first-hand intelligence, or co-produce a corridor briefing, we would like to hear from you.

Erdinc Ekinci Author Co-Director, Founder Institute Japan / Korea / Taiwan Founder, Openfor.co · Founder, Co-Capital Tokyo, May 2026

SOURCES

IMARC Group, "Japan Venture Capital Investment Market Size Report 2025–2034"

Tracxn, "Startups in Japan — 2026 Latest Funding Rounds, Trends and News," January 2026

Chambers and Partners, "Venture Capital 2025 — Japan Trends and Developments"

JETRO, "Global Venture Capital Firms Add Spark to Japan's Startup Ecosystem"

Growth List, "500+ Funded Japan Startups 2026," March 2026

StartupBlink, "Global Startup Ecosystem Index 2025"

CB Insights, "State of Venture 2024 Report"

Coral Capital, published commentary and team profiles, 2024–2025

Disrupting Japan podcast, interview series, 2025

Complex Systems podcast, July 2025

Startup Wired, "Top 10 Startups in Japan to Watch in 2026," January 2026

Global Venturing, "'Big in Japan' is not enough," February 2026

Failory, "Top 73 Venture Capital Firms in Tokyo (2026)"

IncubatorList, "Top VCs & Startup Programs in Japan (2026)"

BaseTemplates, "Top 10 VC Investors in Tokyo in 2026"

Visible.vc, "Exploring the Growing Venture Capital Scene in Japan"

Shizune, "Top 50 VC Funds in Japan in January 2026"

Japan Dev, "Venture Capital in Japan: A Guide to Startup Funding in 2026"

A Co-Capital Ecosystem Report. May 2026. For corrections or contributions, contact the author.

Comments